Following a rather hasty public consultation exercise that ran from 27 December 2016 to 13 January 2017, the Singapore Parliament passed the Companies (Amendment) Bill 2017 on 10 March 2017. On the same day, the Stamp Duties (Amendment) Bill 2017 was also passed with a somewhat similar degree of urgency after the Ministry of Finance sought and obtained the President’s certification. With this, a new stamp duty treatment was introduced for the acquisition and disposal of property holding entities (PHEs). With effect from 31 March 2017, all companies including foreign companies and limited liability partnerships will be required to maintain a register of beneficial owners (termed as registrable “controllers”). When read collectively, the changes seemingly result in a directed aim at a particular group of wealthy individuals buying and selling properties located in Singapore.

A stepped-up buying of properties coincides with the passage of a recent law in Jakarta, also known as the “Tax Amnesty Program”. Surging demand from wealthy Indonesians, was captured by data from Urban Redevelopment Authority and data from private firm Cushman & Wakefield Inc. Disclosure of nationality is voluntary and purchases through foreign companies are not likely to be captured by such data. At the sidelines of the International Tax Conference on 12 July 2017, Indonesian Finance Minister Sri Mulyani Indrawati had estimated that about 60% of S$103.3 billion worth of assets kept abroad by wealthy Indonesians is banked in Singapore. Indeed, some may ask, what better way is there to “bank in” than through the investment of properties in Singapore?

The Move to Raise Stamp Duties Rather Than a Tax on Capital Gains

With the absence of a capital gains tax regime, we have always been regarded as one of the world’s prime location to own property for investment. You are required to pay Buyer’s Stamp Duty (BSD) of 1-3% for documents executed for the sale and purchase of property located in Singapore. BSD will be computed on the purchase price as stated in the document to be stamped or market value of the property (whichever is the higher amount). If you buy or acquire residential properties (including residential land) on or after 8 December 2011, Additional Buyer’s Stamp Duty (“ABSD”) of up to 15% may also be applicable. If you buy or acquire residential properties on or after 20 February 2010, Seller’s Stamp Duty (“SSD”) of up to 16% is payable if the properties are sold within the holding period. We are seeing one of the highest stamp duty rates on buying and selling of properties in the region.

Interestingly, the act of adjusting stamp duties would generally be viewed by the public as a temporary measure when compared to a new legislation to tax gains on sale of properties. Hence there is an inclination to setting up foreign company in holding Singapore property with the effect of avoiding any BSD, ABSD and SSD.

In light of this, the key questions existing and potential property owners should be asking are: is there a structure that optimises my position – should I continue with a structure of foreign company holding Singapore property with the recent changes in stamp duty regulation?

Indirect Acquisition/Disposal of Residential Property

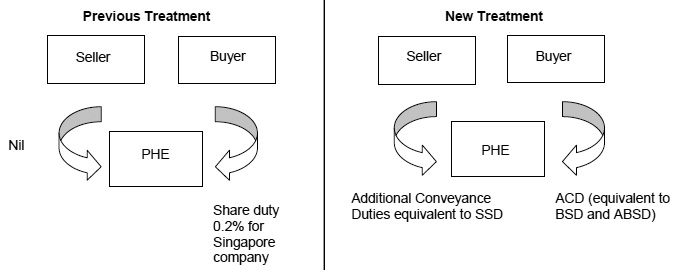

With the new stamp duty treatment targeting indirect acquisition/disposal of residential property via PHE, BSD/ABSD/SSD rates for buyers and sellers are mirrored to the prevailing rates through direct buying/selling. Simply, the aim of the above measures is to bring parity to the stamp duties between the direct buying/selling and indirect buying/selling of residential properties via PHE.

Hence, going forward the same stamp duty rates would apply when you sell the residential property and when you sell the shares of the Singapore company holding the property.

An observer may ask why, if the intention was to put parity to the stamp duties between the direct buying/selling and indirect buying/selling of residential properties, did the government not amend the Stamp Duties Act (“SDA”) to provide parity on other type of properties such as commercial and industrial?

Foreign Company Holding Singapore Residential Property Still Works?

Using a foreign company to hold Singapore residential property instead of a Singapore company certainly has its attractiveness on a stamp duty perspective.

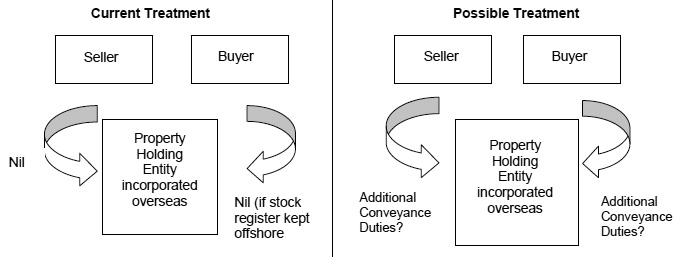

Pursuant to s 36(d) of the SDA, no duty shall be chargeable in respect of any instrument for the transfer on sale of stock issued by or on behalf of corporation, company or body of persons incorporated, formed or established outside Singapore, except where the stock is registered in a register kept in Singapore. Stamp duties are not applicable for indirect buying and selling of residential properties through the foreign entity’s stock by maintaining an offshore register.

To a layman, this would mean that when selling the shares of a foreign company holding a Singapore residential property instead of a direct sale of the same residential property, no stamp duty is applicable.

Requirement to Keep Stock Register Locally

Unbeknownst to many, the Companies Act Provisions Section 365 and 366 apply to a foreign company which carries on business in Singapore. “Carrying on business” includes the administration, management or otherwise dealing with property situated in Singapore as an agent, a legal personal representative, or a trustee, whether by employees or agents or otherwise, including activities carried on without a view to any profit. And if you are caught under these provisions, the foreign company must keep a register of its members at its registered office in Singapore or at some other place in Singapore and lodge a notice with the Registrar specifying the local address at which the register of members is kept (see s 379 of the Companies Act).

Advancement of Duty Point to Signing of Agreement Instead of the Time the Share Transfer Form is Executed

One related change that might have resonated negatively with some of those in the field of mergers and acquisitions is the removal of the exception under s 22(1)(b) of the SDA for contracts and agreements for sale of stock, to be chargeable. The effect of such change is that the duty point for a sale of stock would be at the time of signing of the contract or agreement and not at the point of executing the share transfer form.

In certain foreign jurisdictions, it was understood that no transfer instrument is required to be executed for shares to be transferred. A sale and purchase agreement or some written documents to that effect may be sufficient for the transfer of shares.

Hence this amendment together with the Companies Act Provisions ss 365 and 366 would make the transfer of shares of a foreign company which was previously not dutiable, now dutiable.

For example, in the case of the sale of shares of a BVI company (where the stock register is kept locally) holding a Singapore residential property, once the sale and purchase agreement is signed, relevant Singapore stamp duties would be applicable.

But what is the relevance of the requirement to maintain register of registrable controllers to the stamp duty changes?

Conclusion

It was not long ago when the unprecedented leak of 11.5 million files from one of the largest offshore law firm, Mossack Fonseca, rocked the world. The leaked documents contained personal financial information about wealthy individuals and public officials that had previously been kept private through the use of offshore companies. These examples clearly demonstrated the prevalent practice of wealthy individuals making use of unrelated proxies to deal in offshore companies.

In response to this, the newly legislated s 386AB of the Companies Act defined “controller” as an individual or corporation who has a significant interest in, or significant control over, the company or the foreign company. Although the register of beneficial owners will not be made available to the public, it is subject to inspection by the local authorities upon request. This move appeared to have complemented excellently with new stamp duty treatment as it is always difficult to enforce against stamp duty evasion.

Within a short span of time, the recent changes have addressed not just one point of stamp duty differential between direct buying/selling of properties and indirect buying/selling through companies but at the same time, plugged many gaps in the legislations where buying/selling are carried out using offshore companies, and through proxies.

Perhaps this is the right time to ditch the use of foreign companies to hold Singapore residential properties if the original purpose was to manage the stamp duty exposure efficiently.

► Ho Soon Wing

AscentiaTax Services Pte Ltd

Ho Soon Wing is a tax director of a boutique consultancy firm, AscentiaTax Services Pte Ltd (www.ascentiatax.com), offering comprehensive tax and accounting services to SMEs, including law practices. Soon Wing started his career in the tax practice in a Big 4 accounting firm, working on an extensive portfolio of companies including those in the real estate and hotel industry, infrastructure companies, and government related companies. He has also consulted, as part of the investment management team, on various Fund Structuring and Real Estate Investment Trusts.

Bryan Yew is a director with the Accounting Advisory team in AscentiaTax. Bryan started his audit career in a Big 4 accounting firm with a portfolio of companies mainly in the automotive, construction, research institution and logistics. He was also with the Institute of Singapore Chartered Accountants as the Deputy Head of the Practice Monitoring Department which primary objective was to improve the audit quality in Singapore’s audit firms through the review of their engagement files.

Notes

a. Inland Revenue Authority of Singapore E-Tax Guide “Stamp Duty: Additional Conveyance Duties (ACD) On Residential Property-Holding Entities”

b. Bloomberg’s “Rich Indonesians Snap Up Singapore Homes as Taxman Beckons” By

c. David Roman, Pooja Thakur Mahrotri, and Chanyaporn Chanjaroen

d. Companies (Amendment) Act 2017

e. Stamp duties (Amendment) Act 2017